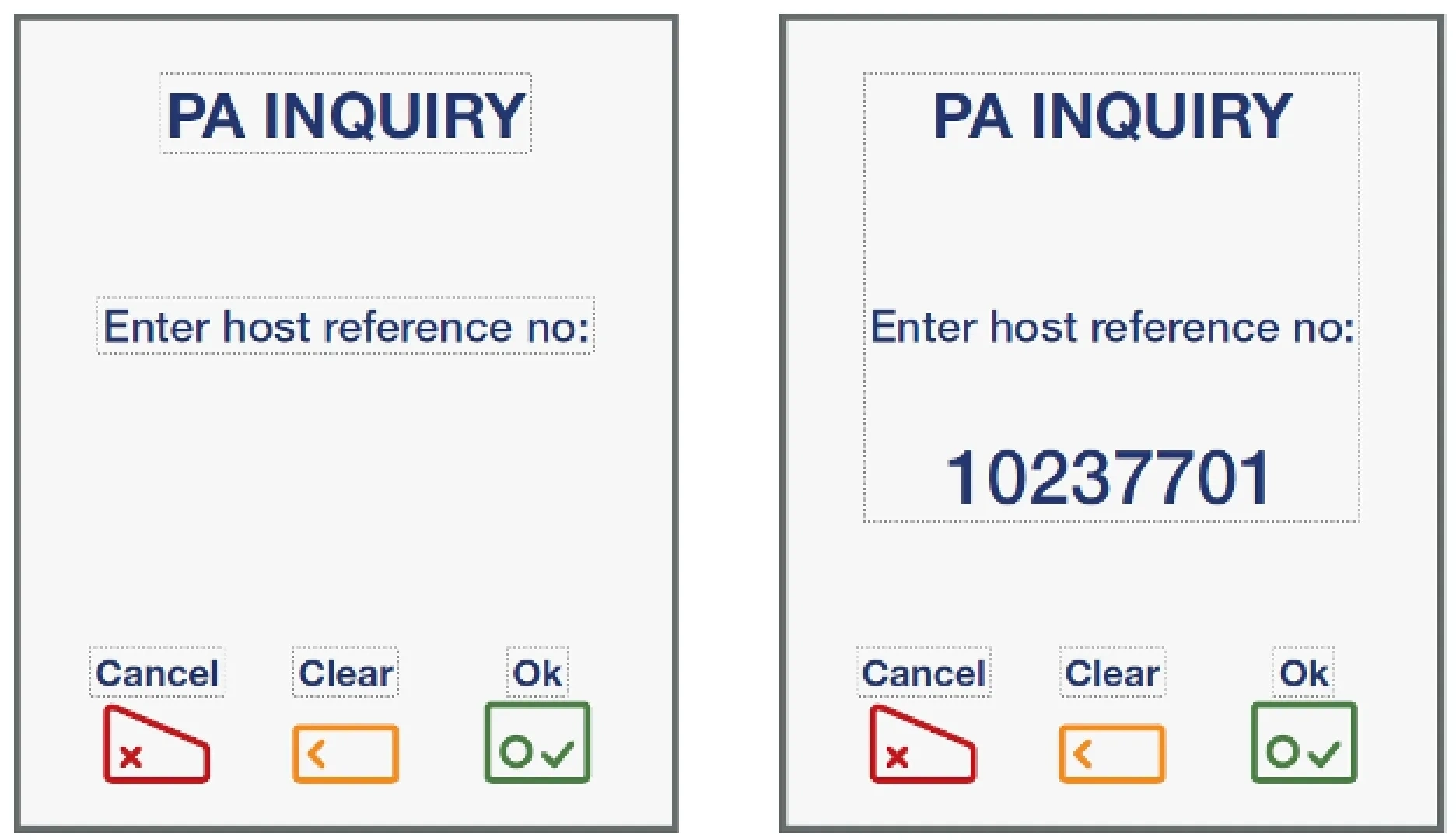

Host Reference Number

Enter the Host Reference Number from the original pre-authorisation transaction and press Enter.

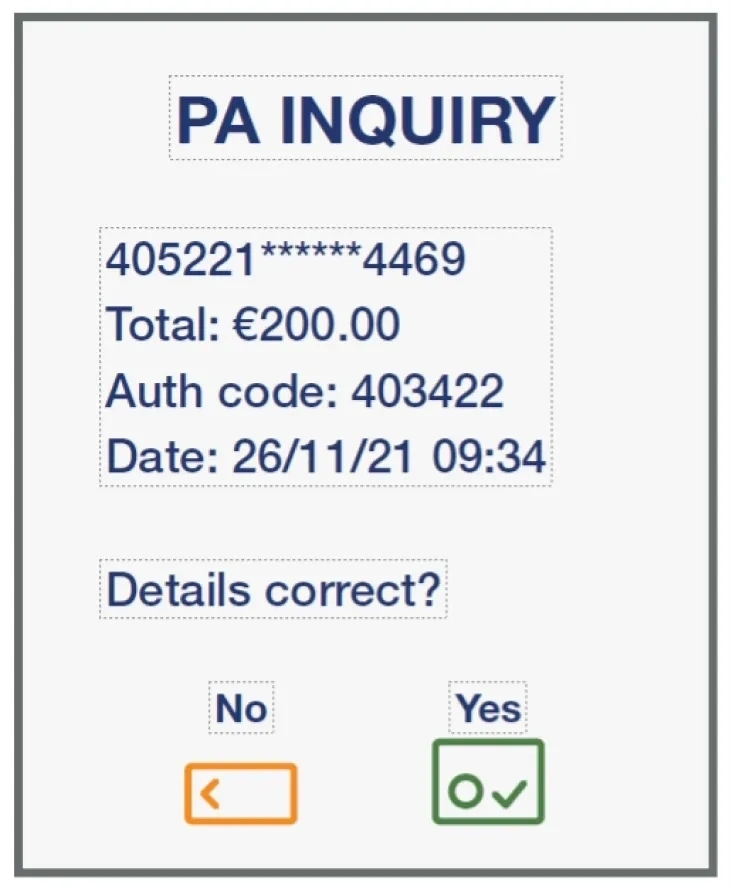

Verify the transaction

The pre-authorisation details will be displayed in your local currency. Verify the transaction details and select Yes.

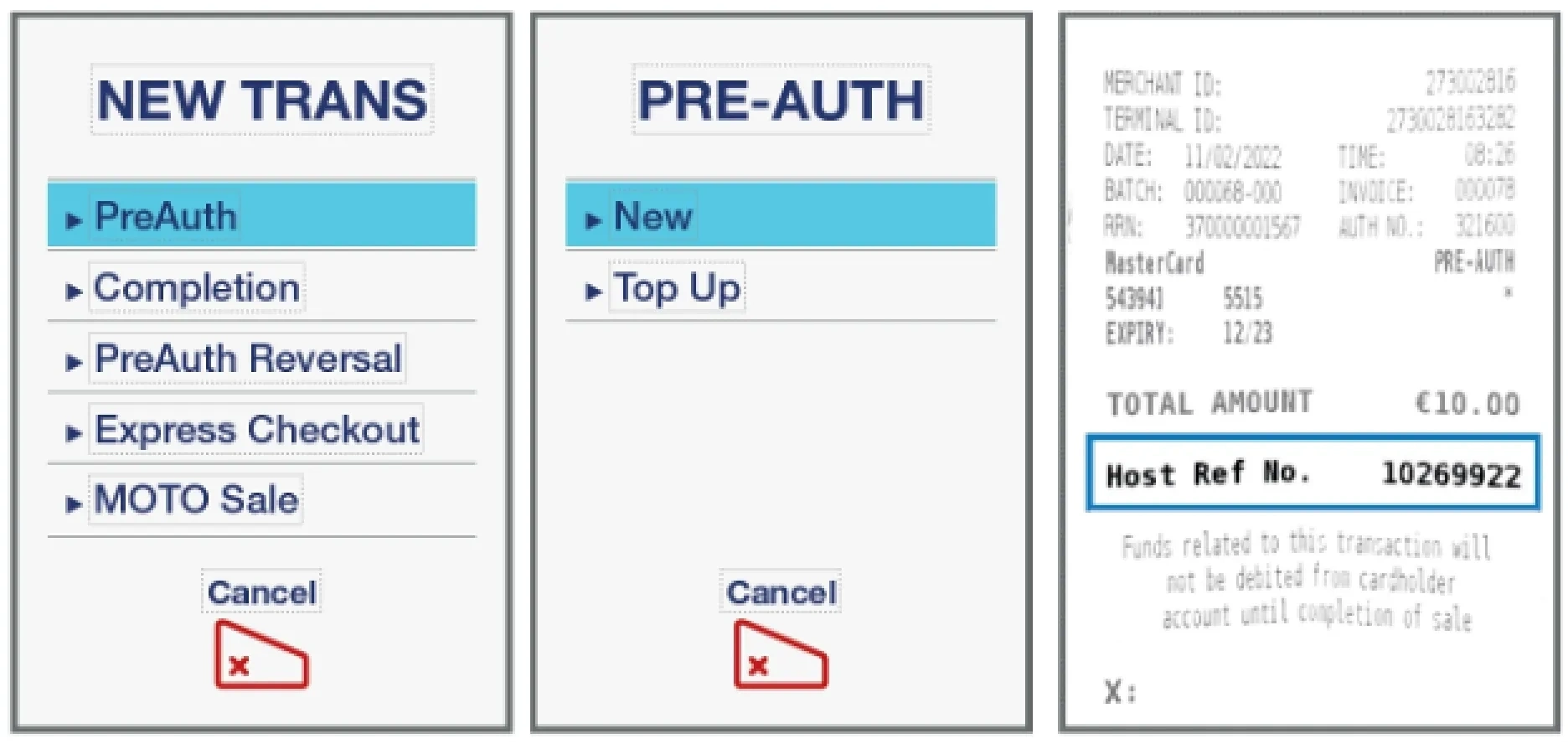

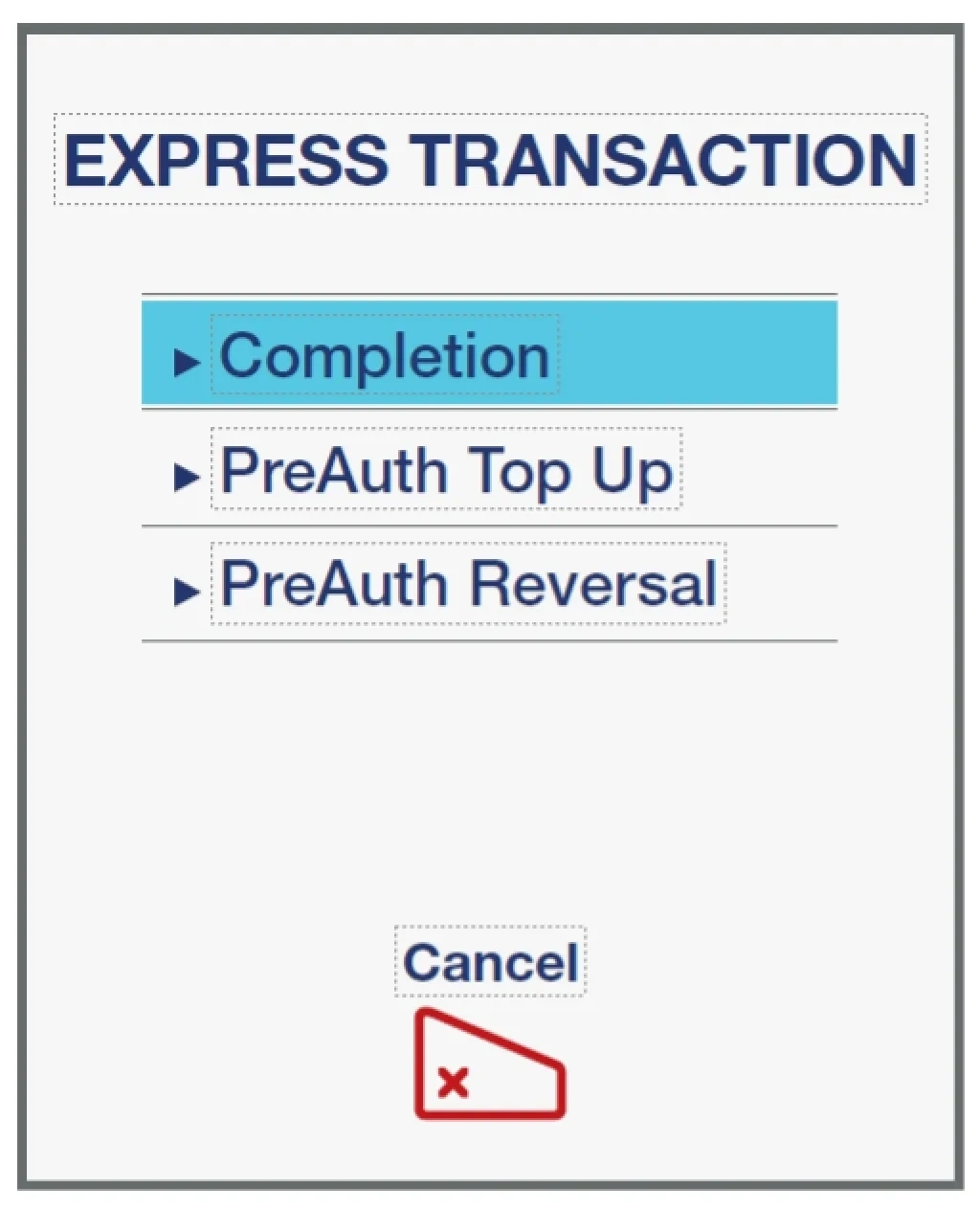

Select Completion or Top Up

Select Completion or Top Up and press Enter.

Enter the completion or Top Up amount

Enter the completion or Top Up amount in your local currency and press Enter.

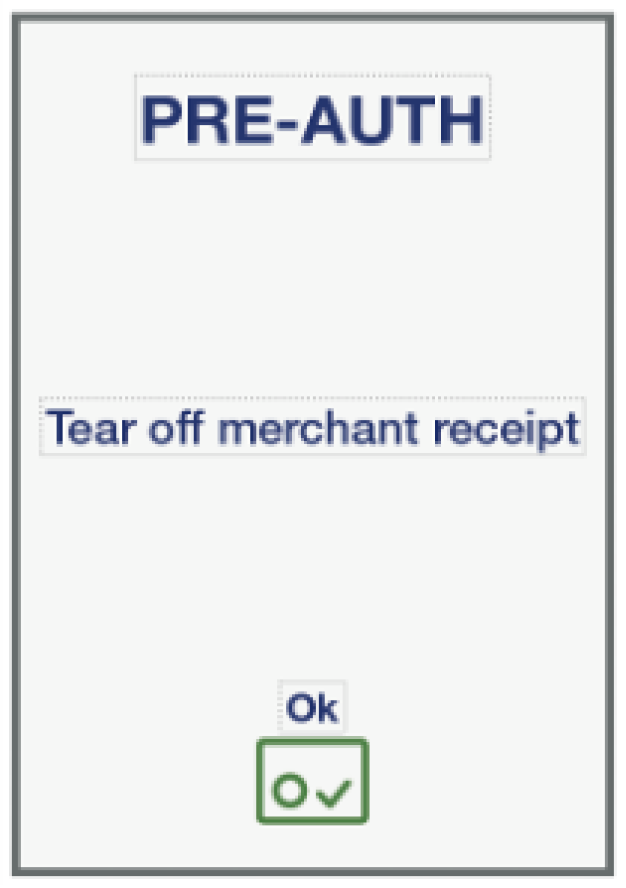

Continue the transaction as normal

Your terminal will verify if DCC was selected

Your terminal will verify if DCC was selected at check in, pre-authorisation or pre-authorisation.

Top Up stages:

- If DCC was selected, the final transaction amount will be printed in the cardholder’s home currency using the current exchange rate.

- If DCC was not selected, the final transaction amount will be printed in the local currency.